8 Bonds

8.1 Present value

A bond is a promise of fixed dollars in the future. Its present value:

PV = \frac{FV}{(1+r)^T}

where FV is the face value at maturity, r is the market interest rate, and T is years to maturity.

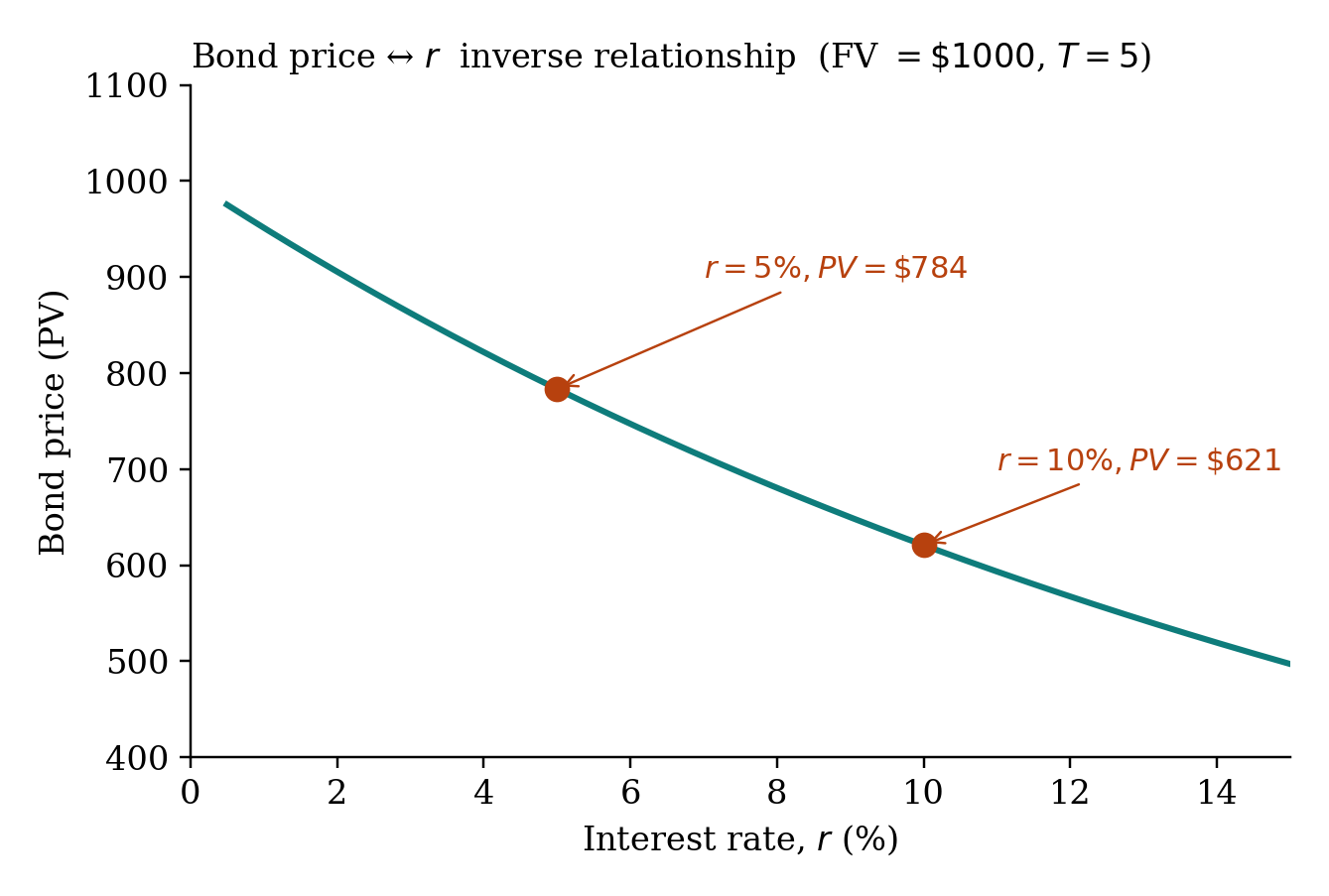

8.2 The inverse relationship

r rises, PV falls. Always. The two cannot move in the same direction.

Why? A bond is a fixed promise of future dollars. If the discount rate rises, those future dollars are worth less today. Equivalently: if new bonds pay 8% and you hold a 7% bond, no one will pay full face value for yours; its market price falls until its yield-to-maturity matches 8%.

8.3 Backing out r

If you know PV, FV, and T:

r = \left(\frac{FV}{PV}\right)^{1/T} - 1

Take the T-th root of FV/PV, subtract 1. For T=2, square root. For T=3, cube root.

8.4 Worked example

FV = \$1{,}000. T = 5 years. At r = 5\%: PV = 1000/1.05^5 = \$783.53. At r = 10\%: PV = 1000/1.10^5 = \$620.92. The bond is worth \$160 less.

8.5 Try it

The bond pricer calculates PV given FV, r, T — and inverts to find r given PV.