7 The money market

7.1 Three motives for money demand

| motive | what drives it | which curve effect |

|---|---|---|

| Transactions | Need money to buy goods. Rises with Y and P. | Shifts M^D when Y or P changes. |

| Precautionary | Buffer against unexpected spending. | Shifts M^D under uncertainty. |

| Speculative | Hold money rather than bonds when bonds look unattractive. Falls with r. | Movement along M^D. |

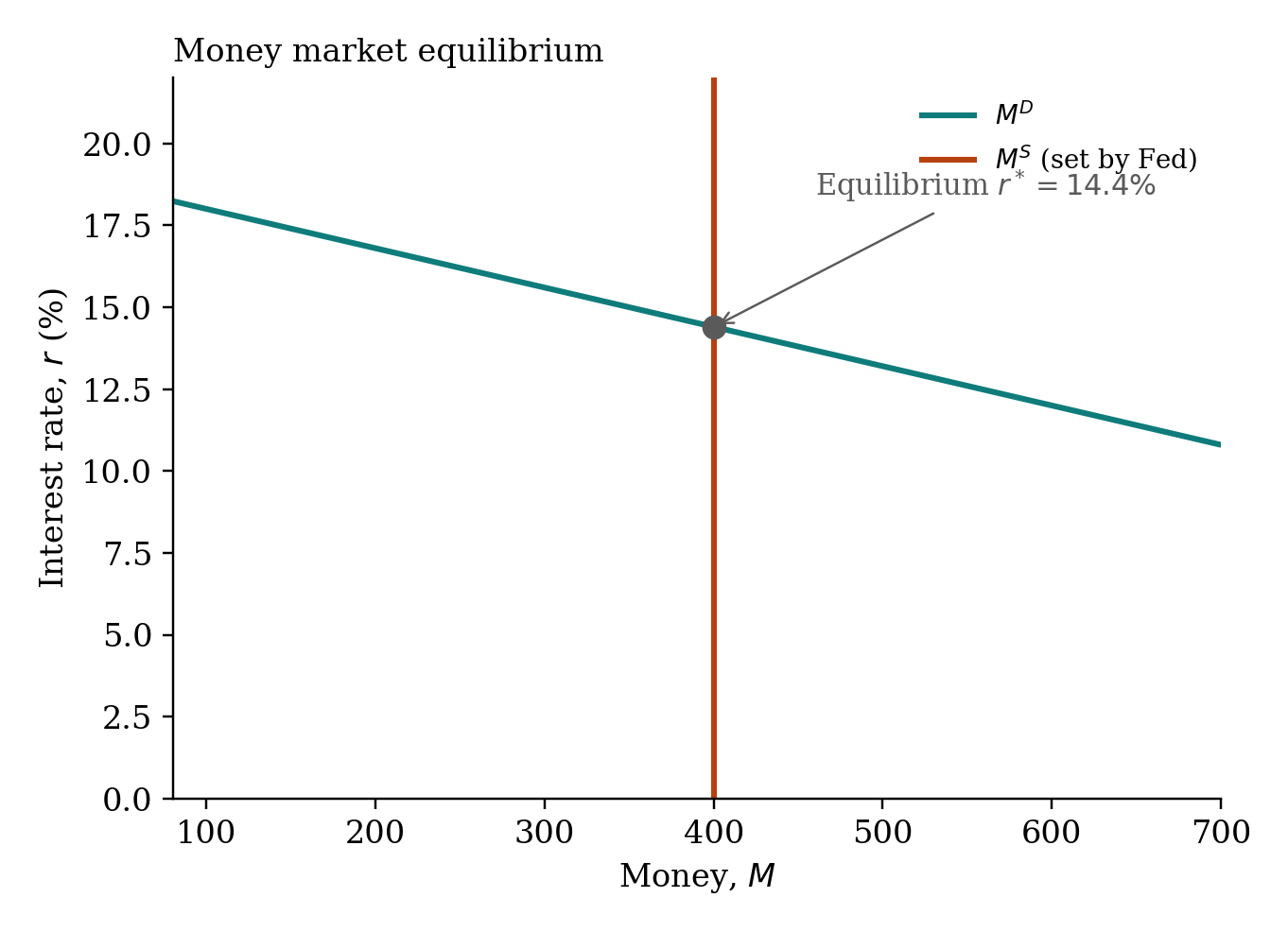

Sum: M^D = f(Y, P, r). Vertical axis r, horizontal M. Downward sloping in r.

7.2 Equilibrium r^*

The Fed sets M^S (vertical line). M^D is the downward-sloping demand curve. r^* is where they cross — but the actual mechanism of adjustment runs through the bond market.

When r > r^*: excess supply of money. People try to reduce money holdings by buying bonds. Bond prices rise. Bond yields fall. r falls toward r^*.

When r < r^*: excess demand for money. People sell bonds for cash. Bond prices fall. Yields rise. r rises toward r^*.

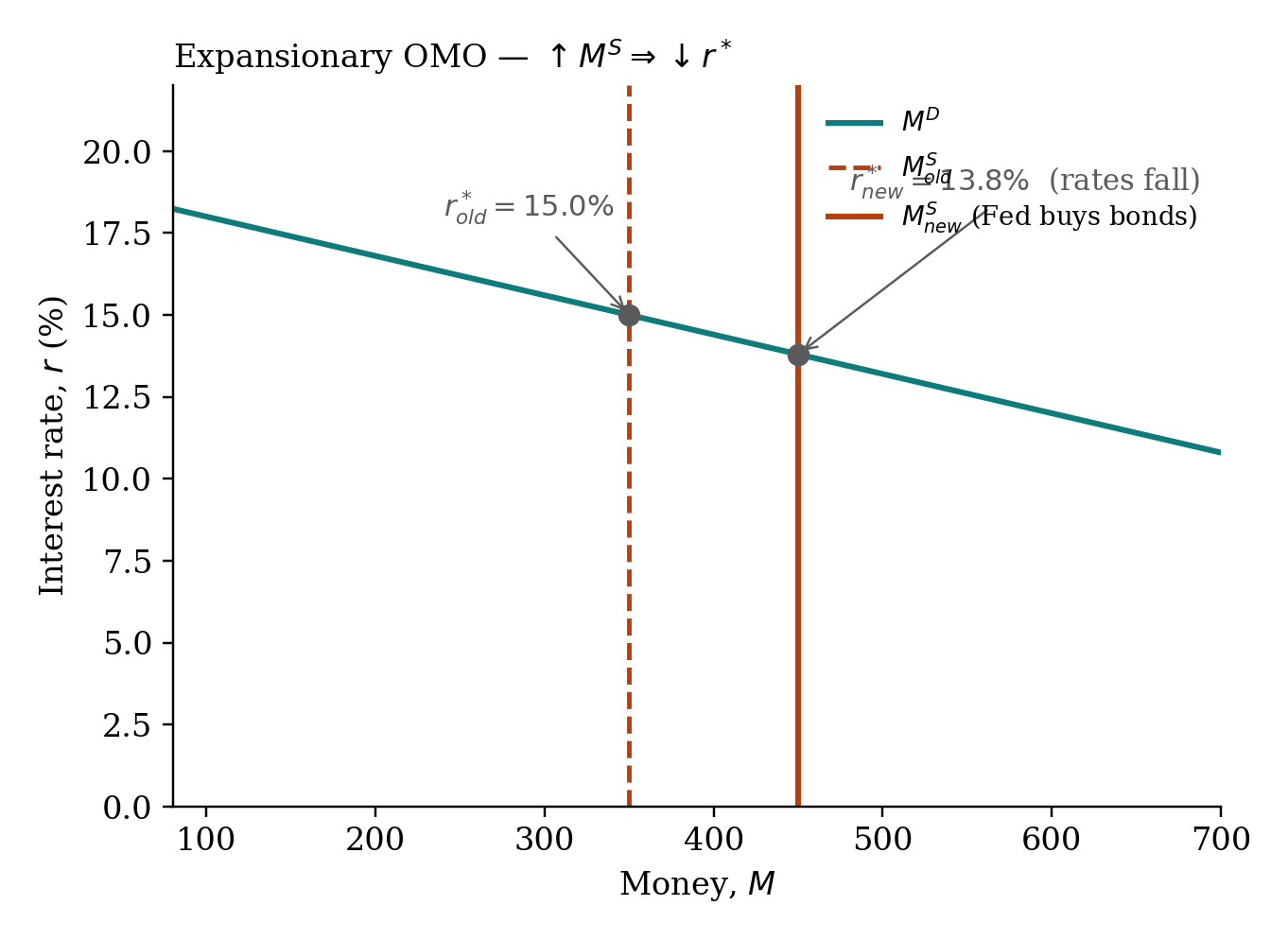

7.3 What moves M^S

Anything the Fed does. OMO purchase shifts M^S right, lowering r^*.

7.4 What moves M^D

Income Y (transactions motive). Price level P (transactions motive). Uncertainty (precautionary). All three shift the curve.

A change in r moves you along the curve, not shift it.

The dual story. “Fed buys bonds, M^S rises, r^* falls” and “Fed bid up bond prices, so the yield-to-maturity fell” describe the same transaction. Money market and bond market are two views of one thing.

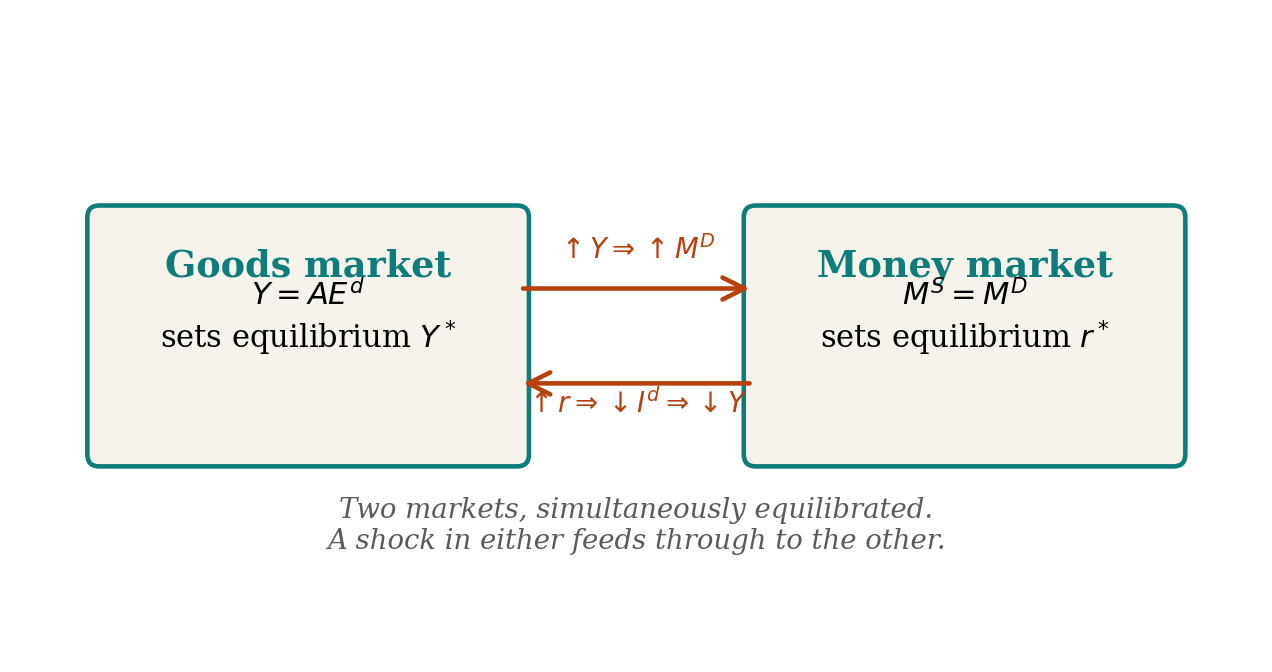

7.5 Goods market \leftrightarrow money market

The two markets equilibrate together.

7.5.1 Monetary policy transmission, end to end

- Fed conducts an OMO purchase.

- \Delta R > 0 \Rightarrow \Delta M^S = K_S \cdot \Delta R > 0.

- \uparrow M^S \Rightarrow \downarrow r^*.

- \downarrow r \Rightarrow \uparrow I^d (firms find more projects profitable).

- \uparrow I^d \Rightarrow \uparrow AE^d \Rightarrow \uparrow Y^* (multiplier K_I).

- \uparrow Y \Rightarrow \uparrow M^D (transactions). r^* rises slightly back. Partial offset.

7.5.2 Fiscal policy transmission

- Government raises \overline{G}.

- \uparrow AE^d \Rightarrow \uparrow Y^* (multiplier K_G).

- \uparrow Y \Rightarrow \uparrow M^D \Rightarrow \uparrow r^*.

- \uparrow r \Rightarrow \downarrow I^d (private investment crowded out).

- The crowding-out partially offsets the original boost. This is why the real-world fiscal multiplier is well below K_G.