The New Markets Tax Credit is the US federal program whose mechanics most closely

match the "blended finance" story you want to tell. The federal government offers

investors a 39% tax credit (claimed over 7 years) in exchange for

putting their equity into a certified Community Development Entity (CDE).

The CDE is a regulated intermediary — usually a bank subsidiary or a nonprofit

community-development financial institution — that re-deploys the money as loans

or equity into qualifying businesses and projects located in low-income census

tracts. Those projects are called QALICBs.

What we observe is the CDE → QALICB flow (the QLICI): who got how much,

where, in which year, and what the total project cost was. The investor-side flow

(QEI, and the tax credit they claim) is upstream and off the public data release.

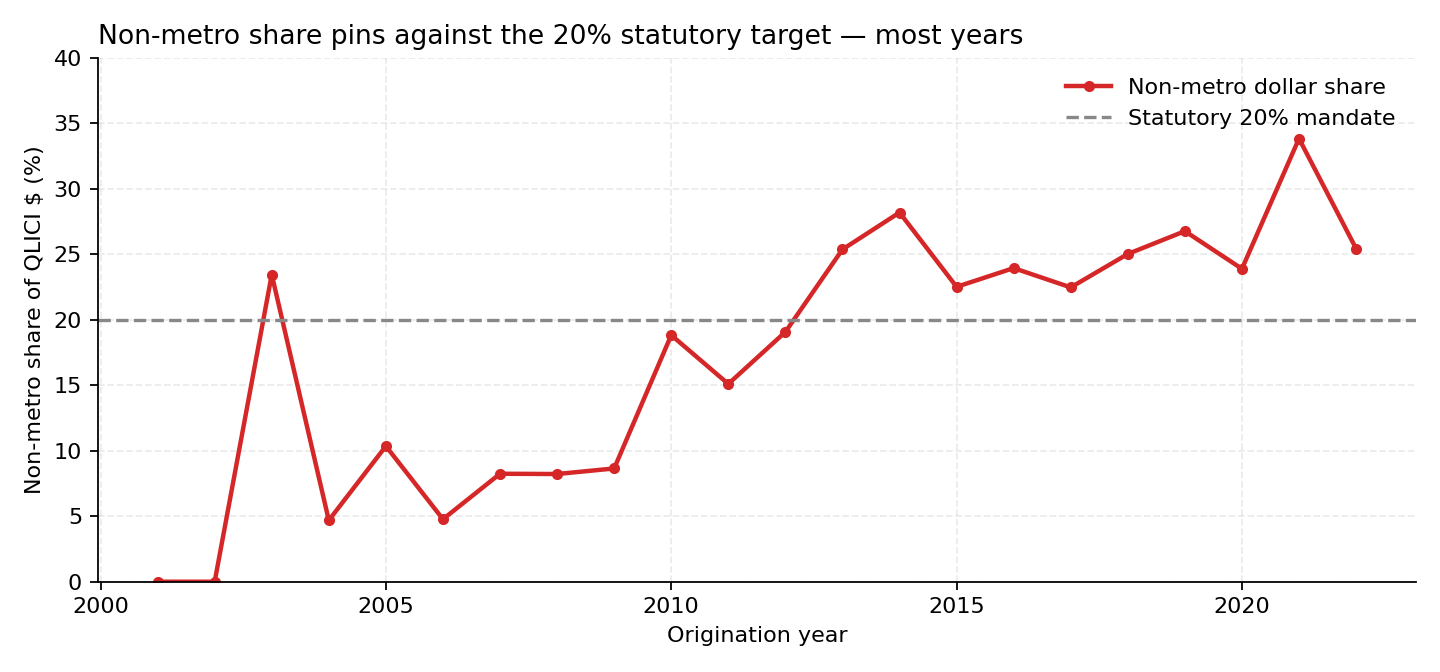

The rural mandate

The NMTC statute requires CDEs to direct at least 20% of their QLICIs to

non-metropolitan census tracts. That creates a testable prediction: CDEs will

bunch against the 20% line unless they have a strong pull to go further.

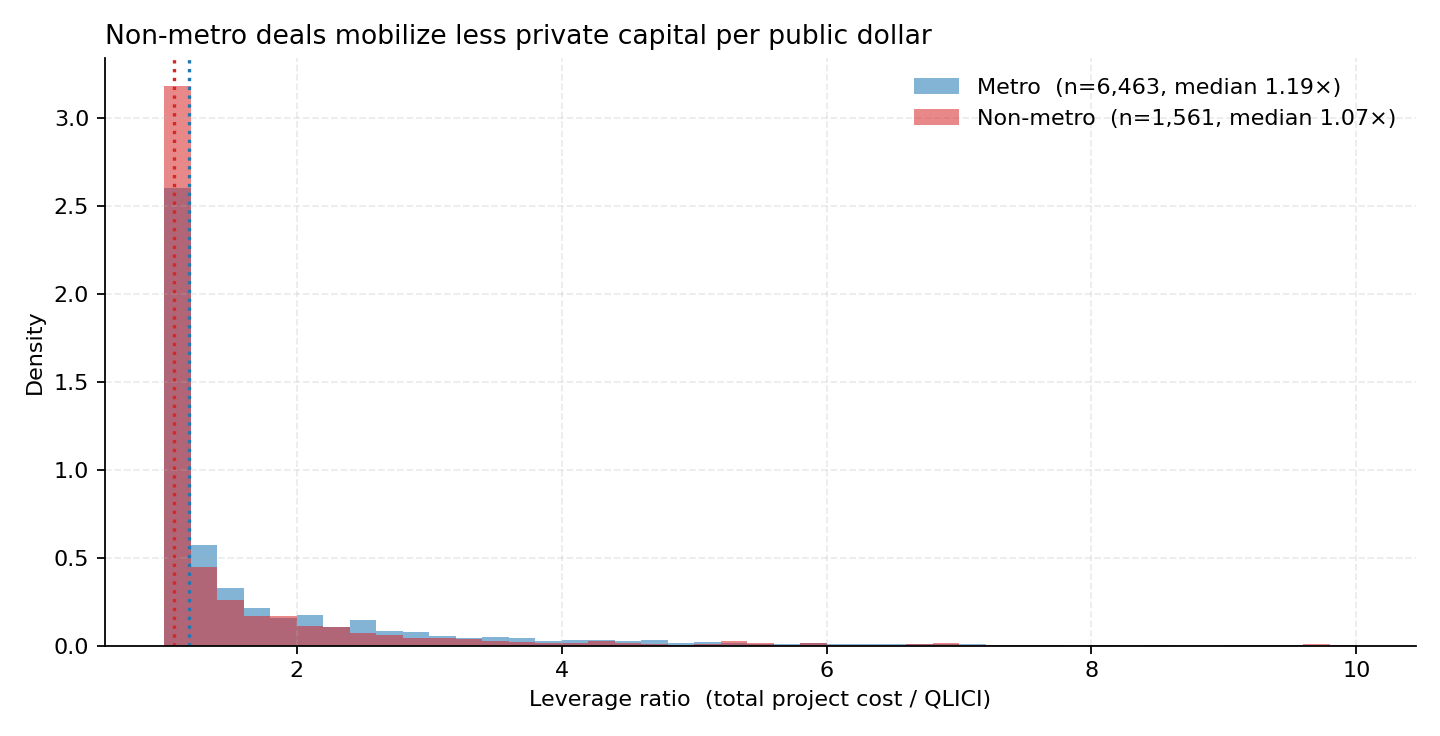

Leverage, as we measure it here

The leverage ratio of a project is total project cost / QLICI. If a $5M

project received a $1M QLICI, it leveraged the federal dollar 5×, meaning $4 of

non-federal capital showed up per $1 of credit. That's the mobilization number.

Why this question is identifiable

Two sharp discontinuities the law gives us for free:

(1) tracts qualify only if poverty ≥ 20% or median family income ≤ 80% of

area median — an RDD cutoff; (2) the 20% rural mandate — a bunching test.

See DATA_DICTIONARY.md for every

column and PROVENANCE.md for SHA-256

hashes, license terms, and a step-by-step recreate-from-scratch recipe.

Every NMTC project, on an Earth map

Each dot is one project, placed at its 2020-census-tract centroid.

Metro · Non-metro.

Dot size ∝ √(QLICI $).

Hover for detail. Scroll-zoom to explore.

— projects · —

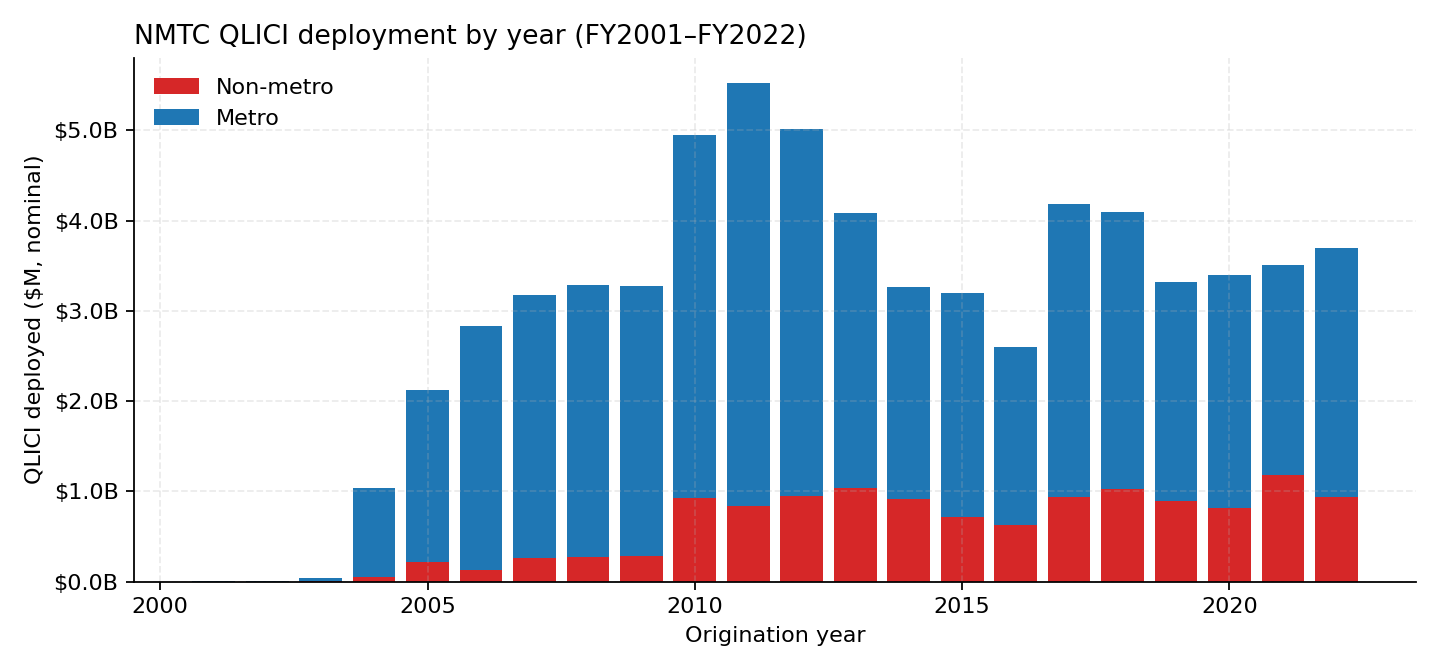

Deployment through time

The program ramped from almost nothing in FY2001 to ~$5 B/yr through the 2010s,

then settled into a $3–4 B/yr steady state. The stacked bar shows metro vs. non-metro

dollar share; the panel below it pulls the non-metro share out as a line, against

the 20% statutory mandate.

Fig 1 · Annual QLICI deployment, metro vs non-metro stacked.Fig 2 · Non-metro dollar share pins the 20% line in most pre-2013 years,

hovers slightly above it thereafter. Classic mandate-binding behavior.

The leverage gap

This is the empirical headline of the first-look brief. Non-metro projects sit

heavier on the 1.0× floor (nearly 100% NMTC-financed, zero private capital

mobilized) while metro projects show a fatter right shoulder (more private debt

and equity stacked on top).

Fig 3 · Leverage-ratio density, metro vs non-metro.

Median metro 1.19× vs. non-metro 1.07×. The gap is small at the median but

the shape tells the story: rural deals rarely stack private capital on top.

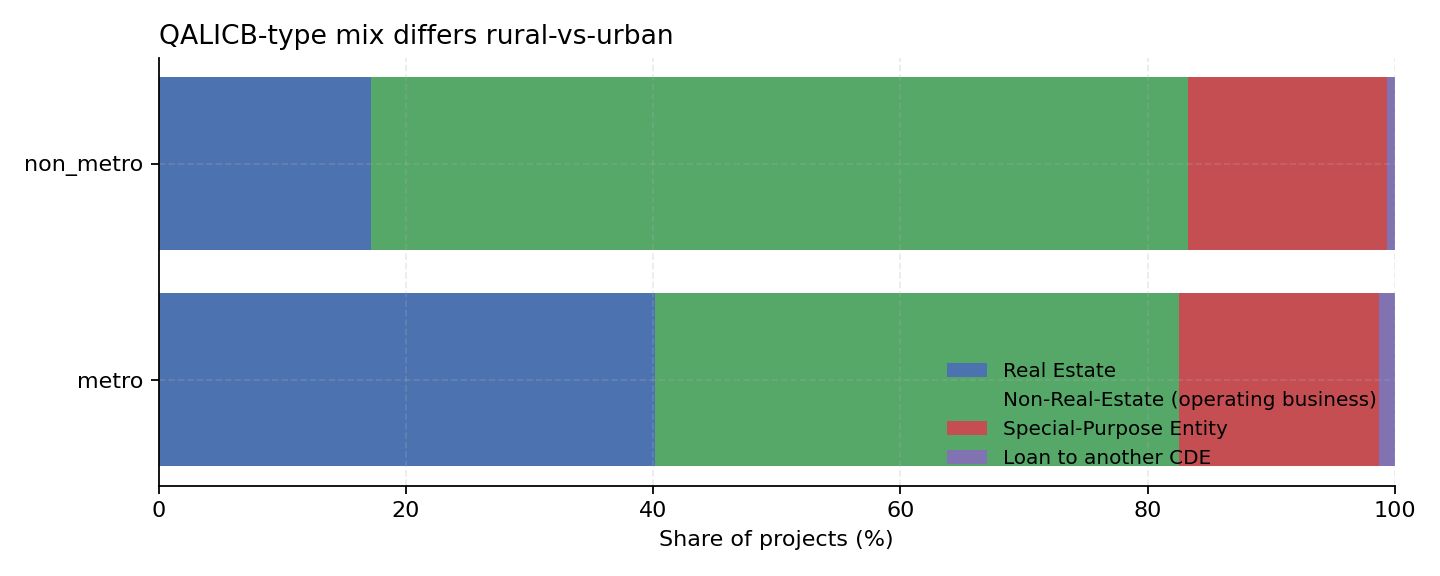

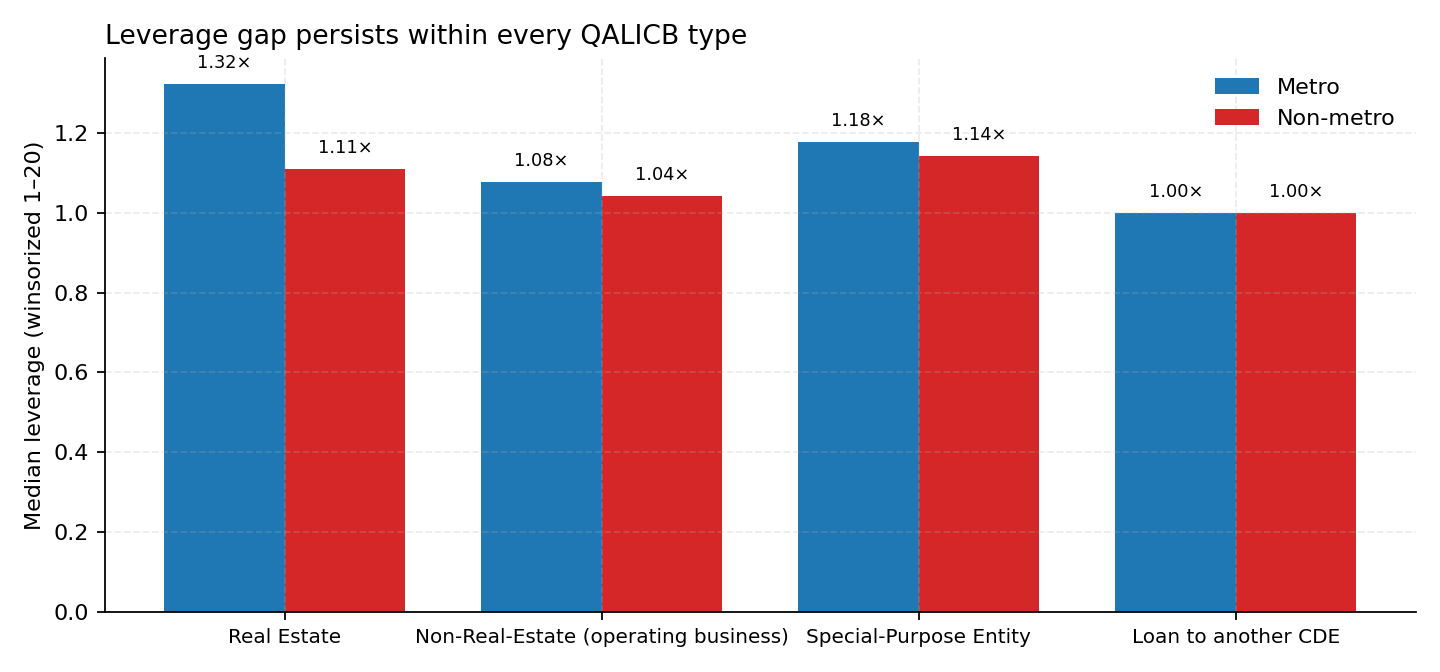

Fig 4 · Metro skews Real-Estate (~40%); non-metro skews operating-business NRE (~65%).

So the leverage gap could be a composition story — except…Fig 5 · …the gap persists within every QALICB type.

It's not composition. It's something about deploying the credit rurally.

CDE-level heterogeneity — the mechanism candidate

Same credit, same 39% federal subsidy, same statute. But the top-20 CDEs — which

together account for more than half of all NMTC dollars — deploy wildly differently

along the rural margin. This is where the paper probably lives.

CDE

QLICI $M

tx

non-metro share

deployment

Sorted by non-metro share (descending). The top row — Rural Development Partners LLC

at ~80% non-metro — and the bottom few (ESIC, Consortium America, Capital Impact) at

<5% are the same federal instrument deployed to different worlds. A within-CDE

fixed-effects specification absorbs that selection.

What the econometrics look like

Four specifications, all identifiable from the public release plus a routine

Census-tract merge.

and the brief reports $\hat\beta \approx -0.26$ (mean) or $-0.12$ (median,

via a quantile regression). But that's contaminated by which CDE

deploys where and what type of project. The fixed-effects version:

with $\gamma_{c(i)}$ a CDE fixed effect, $\delta_{t(i)}$ origination-year,

and $\eta_{q(i)}$ a QALICB-type fixed effect. The quantity of interest is

whether $\hat\beta$ survives the CDE fixed effect — i.e. does the same

CDE mobilize less private capital in non-metro than in metro?

3 · The LIC-eligibility regression discontinuity

A census tract is NMTC-eligible if either condition holds:

where $Y_\ell$ is, say, tract-level NMTC dollars per capita or mean leverage.

$\hat\tau_{R=\text{metro}}$ vs. $\hat\tau_{R=\text{non-metro}}$ is exactly the

"does the policy bite differently in rural markets" question.

4 · The 20% mandate — a bunching test

Let $s_j$ be CDE $j$'s realized non-metro share of QLICIs. The statute requires

$s_j \ge 0.20$. Under no-mandate counterfactual, $s_j$ would be smooth around

$0.20$. Under a binding mandate, we expect a visible mass at $s_j = 0.20$.

Formally, compare the empirical density $\hat f(s)$ to a polynomial fit that

excludes a window around the cutoff:

$B > 0$ is the "excess mass" due to the mandate — standard Chetty et al. (2011) /

Kleven (2016) machinery. CDEs that exceed the mandate voluntarily reveal

willingness-to-deploy rurally; CDEs that pin the mandate are constrained.

The marginal rural project identifies off the constrained CDEs.

5 · Putting it together

The empirical paper is short: (2) establishes that the rural gap isn't a

composition artefact (CDE FE absorbs identity, QALICB FE absorbs type);

(3) shows that the RDD treatment effect differs between metro and

non-metro (the interaction we care about); (4) validates the identifying

assumption by showing CDEs bunch exactly where the law says they would.

Where to go next — three moves

Census-tract merge (this week). Join tract FIPS to 2016–2020 ACS

poverty + MFI + population + USDA RUCA codes. That gives us the RDD running

variable ($P_\ell - 0.20$) and a continuous rurality gradient (RUCA 1–10)

instead of the binary metro flag.

CDE-type classification (this week). Hand-classify the top 50

CDEs by institutional form — bank subsidiary / nonprofit CDFI / for-profit

specialized / government. Turns "CDE variation" from a name into a

structural variable we can interact with rural.

First-look figure (next week). Binned scatter of project-level

leverage vs. tract poverty rate, metro and non-metro overlaid. If the

discontinuity is visible at the 20% poverty threshold for both subgroups

but the rural slope is flatter, the paper is real.